After-Tax 401(k) Contributions Part I: Making the Most of Your Solo 401(k) Space

Be sure to read to the end for a special trivia question!

However, if you want to actually get paid, make sure you are in network for the White After-Tax Grimace’s health insurance.

Note: This is the first of a two-part series. Today’s blog post will cover some of the benefits of making after-tax 401(k) contributions, on a high level. Part II will talk about the interaction with cash balance plan contributions and pitfalls to the overall strategy.

Overview of After-Tax 401(k) Contributions

Most physicians have at least heard of the Backdoor Roth IRA.

The basic idea is that high-income taxpayers often make too much money to contribute directly to a Roth IRA. However, they may still be able to make a non-deductible contribution to a traditional IRA and then convert it to a Roth IRA.

There is a similar strategy available inside some 401(k) plans. It is commonly called the Mega Backdoor Roth.

The name makes it sound like something cooked up in a tax shelter laboratory. In reality, the concept is not that exotic. You make after-tax, non-Roth employee contributions to a 401(k), then convert those contributions to Roth. The conversion can happen inside the plan if the plan allows in-plan Roth conversions, or it can happen by rolling the money to a Roth IRA if the plan allows in-service distributions.

The hard part is not understanding the basic idea.

The hard part is having a plan that actually allows it.

Most employer 401(k) plans do not allow this strategy. For it to work well, the plan generally needs to allow two things:

After-tax employee contributions, above and beyond the regular employee deferral limit.

Either in-plan Roth conversions or in-service rollovers to a Roth IRA.

That combination is not especially common.

There are a few reasons for this. First, after-tax employee contributions can create nondiscrimination testing problems. Employer plans generally need to make sure the plan does not disproportionately benefit owners and highly compensated employees. If only the highest earners are interested in making large after-tax contributions, the plan can fail testing.

Second, these features add cost and complexity.

Third, if you work for a large hospital system, there may simply not be enough demand. A small subset of financially savvy, high-income doctors may be clamoring for a Mega Backdoor Roth feature, but most employees are content to make their regular employee deferral and receive the employer match.

However, if you are self-employed, you may have more control. You can choose a custom 401(k) plan that includes these features.

There is a catch. Most free or low-cost solo 401(k) plans from mainstream providers are fairly basic. A custom plan with after-tax contributions and Roth conversion features will likely cost hundreds of dollars to set up and maintain each year.

That does not mean it is a bad idea. It just means the strategy needs to be worth the administrative hassle.

If you are a self-employed physician and you do not have the cash flow or desire to contribute beyond the standard employee and employer contribution limits, there probably is not much point in paying for a plan with extra bells and whistles.

But for the right physician, this can be a powerful planning tool.

The Annual Additions Limit: The Limit Most People Don’t Know About

Most people know there is a limit on how much they can put into a 401(k) as an employee.

For 2026, that employee deferral limit is $24,500 if you are under age 50.

But there is another limit that matters just as much for this discussion: the annual additions limit.

This is the maximum amount that can go into a defined contribution plan, such as a 401(k) or solo 401(k), for a participant from all sources during the year. That includes employee deferrals, employer contributions, after-tax employee contributions, and forfeitures.

For 2026, the annual additions limit is $72,000 for someone under age 50.

Here is why this matters.

Suppose you are employed by a hospital system and max out your employee deferral there. You have already used your $24,500 employee deferral limit for the year.

Now suppose you also have self-employment income from expert witness work, consulting, telemedicine, locums, or a side practice. You set up a solo 401(k) for that business.

Since you already used your employee deferral at your main job, you generally cannot make another regular employee deferral to your solo 401(k). The employee deferral limit is shared across plans.

However, you may still be able to make an employer contribution to the solo 401(k).

For an S corporation, the employer contribution is generally based on W-2 wages from the S corporation. For a sole proprietor, the calculation is more nuanced because it is based on adjusted self-employment income. This is one of the reasons you should not wing the calculation.

Either way, the employer contribution may not get you anywhere close to the $72,000 annual additions limit.

This is where after-tax 401(k) contributions can be helpful.

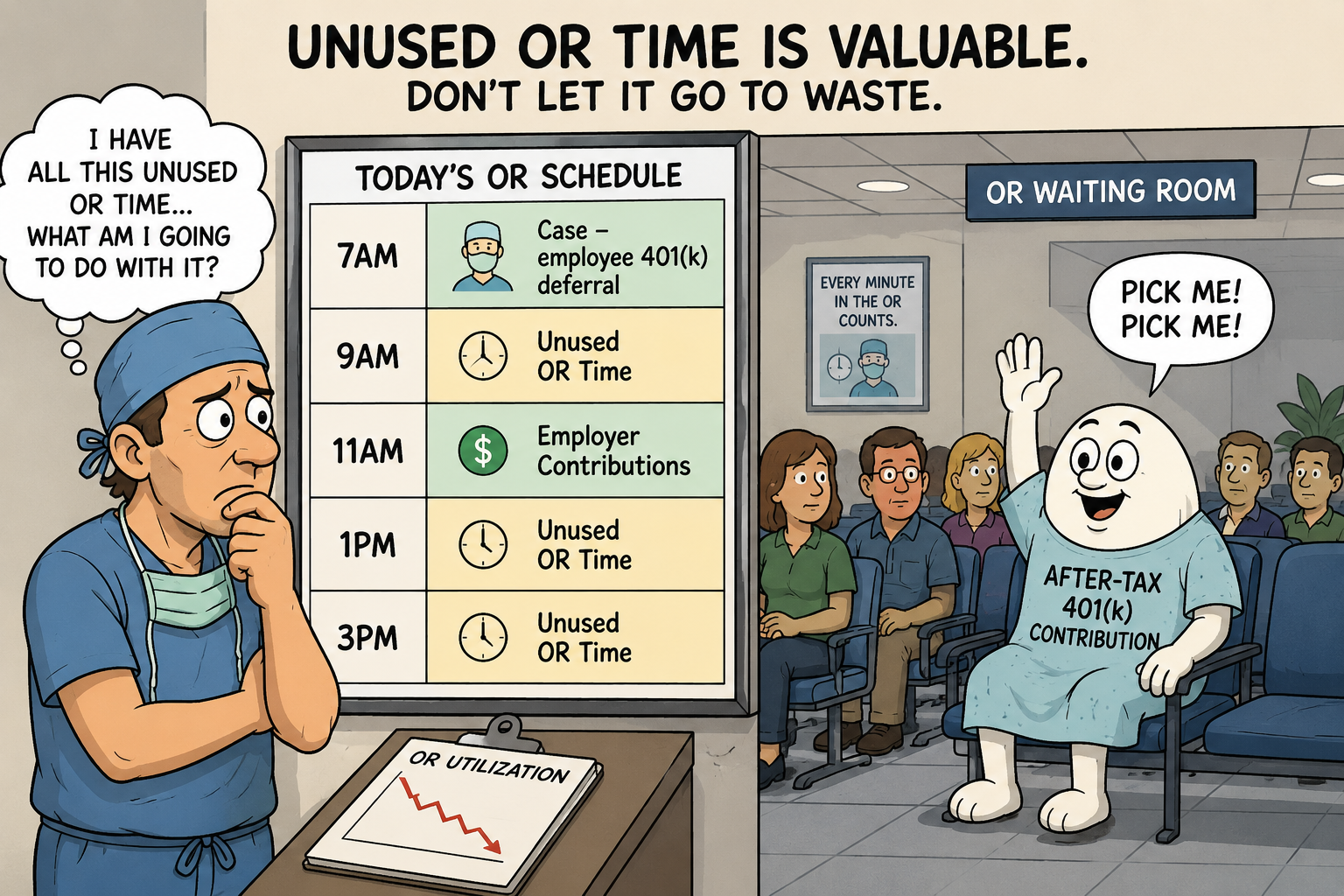

Unused solo 401(k) space is like unused time in the OR. The capacity was reserved for you, but if you don’t use it before the schedule closes, you can’t go back and operate in yesterday’s empty slot.

If the plan allows after-tax employee contributions, you may be able to fill the gap between what you contributed as an employee, what the business contributed as an employer, and the $72,000 annual additions limit.

An Example

Suppose Dr. Smith is under age 50 and has a W-2 job at a hospital. She maxes out her hospital 401(k) with a $24,500 employee deferral.

She also works as a sole proprietor, and her calculated compensation is $100,000.

She may be able to make an employer contribution of up to $25,000, assuming the plan rules are satisfied.

Without after-tax contributions, her solo 401(k) contribution may stop there.

But if her custom solo 401(k) allows after-tax employee contributions, she may be able to contribute more. The annual additions limit is $72,000. If she has $25,000 of employer contributions to the solo 401(k), there may be substantial remaining room.

That remaining room can potentially be filled with after-tax employee contributions, depending on the plan terms, compensation, and other facts.

In other words, no empty slots on the OR schedule.

This is why the “Mega” in Mega Backdoor Roth matters. A regular Backdoor Roth IRA is usually measured in thousands of dollars per year. A Mega Backdoor Roth strategy may allow tens of thousands of additional dollars to move into Roth accounts each year.

Why Would a High-Income Doctor Want Roth Money?

A reasonable objection is that most doctors in their peak earning years prefer pre-tax contributions.

If you are in a high tax bracket today and expect to be in a lower tax bracket in retirement, pre-tax retirement contributions can make a lot of sense. You take the deduction now, invest the tax savings, and pay tax later when your rate may be lower.

But not every physician is in the same situation. This is why I don’t like blanket statements such as “do pre-tax if you’re a doctor” or “Roth is always better because tax-free growth is amazing.”

The better question is: what is your actual marginal tax rate now, and what do you reasonably expect it to be later?

And by marginal tax rate, I do not just mean the federal tax bracket printed on a chart. State taxes, student loan payments, phaseouts, QBI, credits, Medicare premiums, and other moving pieces can all change the answer.

More on marginal tax rates: Why Your Marginal Tax Rate Isn’t 24%

The QBI Deduction Twist

The Qualified Business Income deduction allows some business owners to deduct up to 20% of qualified business income.

This creates an interesting wrinkle.

Suppose you make a $10,000 deductible employer contribution to a solo 401(k). That deduction may reduce your business income by $10,000. If you are eligible for the full QBI deduction, reducing business income by $10,000 may also reduce your QBI deduction by $2,000.

That does not mean the 401(k) contribution is bad. It just means the deduction may not be worth quite as much as you think.

For example, if you are in the 24% federal bracket, you may assume a $10,000 deduction saves $2,400 of federal tax. But if it also reduces your QBI deduction by $2,000, the net reduction in taxable income is only $8,000. At a 24% rate, that is $1,920 of federal tax savings, not $2,400.

In effect, the deduction is only worth 80% as much as the tax bracket alone would suggest.

This is one reason after-tax employee contributions can be appealing. They are not deducted by the business. They do not reduce QBI in the same way an employer contribution does. If they are promptly converted to Roth, they may function similarly to Roth contributions while preserving more QBI deduction.

The devil is absolutely in the details, but this is the general idea.

TaxSmart Takeaway

The Mega Backdoor Roth is not magic. It is a way to use after-tax 401(k) contributions and Roth conversions to fill unused space inside a retirement plan.

For self-employed physicians with strong cash flow, a properly designed plan, and room above their regular employee and employer contributions, it can allow far more money to move into Roth accounts than a regular Backdoor Roth IRA.

The tax analysis also needs to be individualized. Pre-tax contributions are often attractive for high-income physicians, but QBI, state taxes, tax diversification, future retirement income, and temporary income changes can all shift the math.

Unused 401(k) space is like unused OR time. It may be valuable, but only if the schedule, staff, and patient are all lined up correctly.

Special Trivia Question!

Imagine you open a Solo 401(k) and contribute the annual additions limit at the end of every year from 2026 - 2035.

The annual additions limit increases by $1,500 every year with inflation (It is $72,000 in 2026, and $85,500 in 2035).

The investments grow 8% in value annually.

After 2035, your plan is to work part-time just enough to cover expenses, and then retire completely after 2045.

What is the value of the Solo 401(k) account at the end of 2035 (rounding to nearest $100k)?

A. $1.6 million

B. $2.1 million

C. $2.4 million

D. $2.8 million

Click here for the answer!