The §469 Grouping Election: A Planning Tool for Physicians Who Own Their Office Building

Many physicians eventually reach the point where they own both a medical practice and the real estate used by that practice. This is common for practice owners who operate from a dedicated office, clinic, or professional building. The structure often looks like this: the doctor owns the medical practice through an S corporation, partnership, or professional entity, and the building is owned separately, often through an LLC. The practice pays rent to the building entity, the building reports rental income and expenses, and everyone moves on. It seems simple enough, but from a tax standpoint, this arrangement raises an important question: is the rental activity passive or non-passive?

Why Does My Tax Professional Charge So Much? A Physician’s Guide to Lowering Your Tax Prep Bill

So if you’ve ever wondered, “Why does my tax professional charge so much?” or “Why did my fee go up this year?” this post is for you.

The short answer is this: complexity takes time, and during tax season, time is the scarcest resource in the building.

The good news? There are practical ways to make your return easier, cleaner, and sometimes less expensive to prepare.

After-Tax 401(k) Contributions Part II: Pitfalls and Interactions with Other Retirement Plans

After-tax 401(k) contributions become especially interesting when paired with a cash balance plan. A cash balance plan may allow very large pre-tax contributions, while after-tax 401(k) contributions may help prevent unused defined contribution plan space from going to waste. For high-income physicians with the right facts, the combination can be one of the most powerful retirement planning strategies available.

After-Tax 401(k) Contributions Part I: Making the Most of Your Solo 401(k) Space

Most physicians have at least heard of the Backdoor Roth IRA.

The basic idea is that high-income taxpayers often make too much money to contribute directly to a Roth IRA. However, they may still be able to make a non-deductible contribution to a traditional IRA and then convert it to a Roth IRA.

There is a similar strategy available inside some 401(k) plans. It is commonly called the Mega Backdoor Roth.

Claim of Right (§1341): What Happens When You Have to Pay Back a Signing Bonus?

One of the most common “golden handcuffs” physicians face is the signing bonus.

It looks great up front. It often feels like free money. However, many hospital systems only offer these because they need to sweeten the pot to get doctors to accept their offers. For that reason, it’s best not to assume that this will be your “forever job,” and it is also beneficial to save enough cash to repay part of the signing bonus, should you exit early.

Time To Buy a Home? Here’s What Actually Happens to Your Taxes

For most physicians, the decision to buy a home is driven by lifestyle, not taxes.

That said, once you cross into higher income levels, the tax treatment of homeownership can become meaningful—especially when itemized deductions come into play.

This post walks through what actually changes when you go from renting to owning, and where the real planning opportunities exist.

The “Double Phase-Out” of the QBI Deduction (and Why It Matters for S Corps)

If you’re a physician, the Qualified Business Income (QBI) deduction can feel like a moving target.

Below a certain income level, the deduction is straightforward and valuable. Above it, the deduction disappears entirely.

But in between, things get more complicated.

There is a middle zone where the deduction doesn’t just phase out—it can get reduced from multiple angles at once. Understanding how that works is important, especially when evaluating whether an S corporation election makes sense.

How Are Inheritances Taxed? (And How to Plan for Them)

Most people don’t spend much time thinking about how an inheritance will be taxed—until it actually happens.

From a tax standpoint, inheritances are a bit counterintuitive. In many cases, nothing dramatic happens right away, but over time—especially with retirement accounts—the tax consequences can be significant.

If you’re expecting to inherit assets (or already have), here’s how to think about it.

Is That Drive Deductible? The Rules Every 1099 Physician Should Know

For many self-employed physicians—especially locums, telehealth doctors, and those working at multiple sites—vehicle expenses are one of the most misunderstood deductions in the tax code.

IRS Publication 463 lays out the rules. The principles are straightforward, but the real value comes from understanding how to apply them in real life—and how to plan ahead.

Let’s walk through it.

How Bad Is the Pro Rata Rule, Really?

The pro rata rule is often described as the “death blow” to the backdoor Roth IRA. In reality, it’s not nearly as bad as many physicians assume. In some cases, it simply forces you to think more strategically about timing and tax brackets.

Let’s break it down.

Work Off the Beaten Path? Don’t Miss Out on These 7 State Rural Practice Credits

Now that it’s tax filing season, many taxpayers (especially self-employed ones) are looking at their draft 1040’s and feeling sticker shock. Unfortunately, your options for reducing your tax bill at this stage of the game are pretty limited, but it’s worth looking into whether you qualify for any unexpected tax credits at the federal, and especially the state level.

Gambling Losses, Taxes, and the One Big Beautiful Bill: When the House (and Uncle Sam) Always Wins

Gambling taxes have always been a little strange. If you’ve ever wondered why you can “break even” at the casino but still lose money after taxes, you’re not imagining things.

With the passage of the One Big Beautiful Bill (OBBBA), those rules have changed again—this time in a way that makes gambling less punitive for some taxpayers, but possibly slightly more so for others.

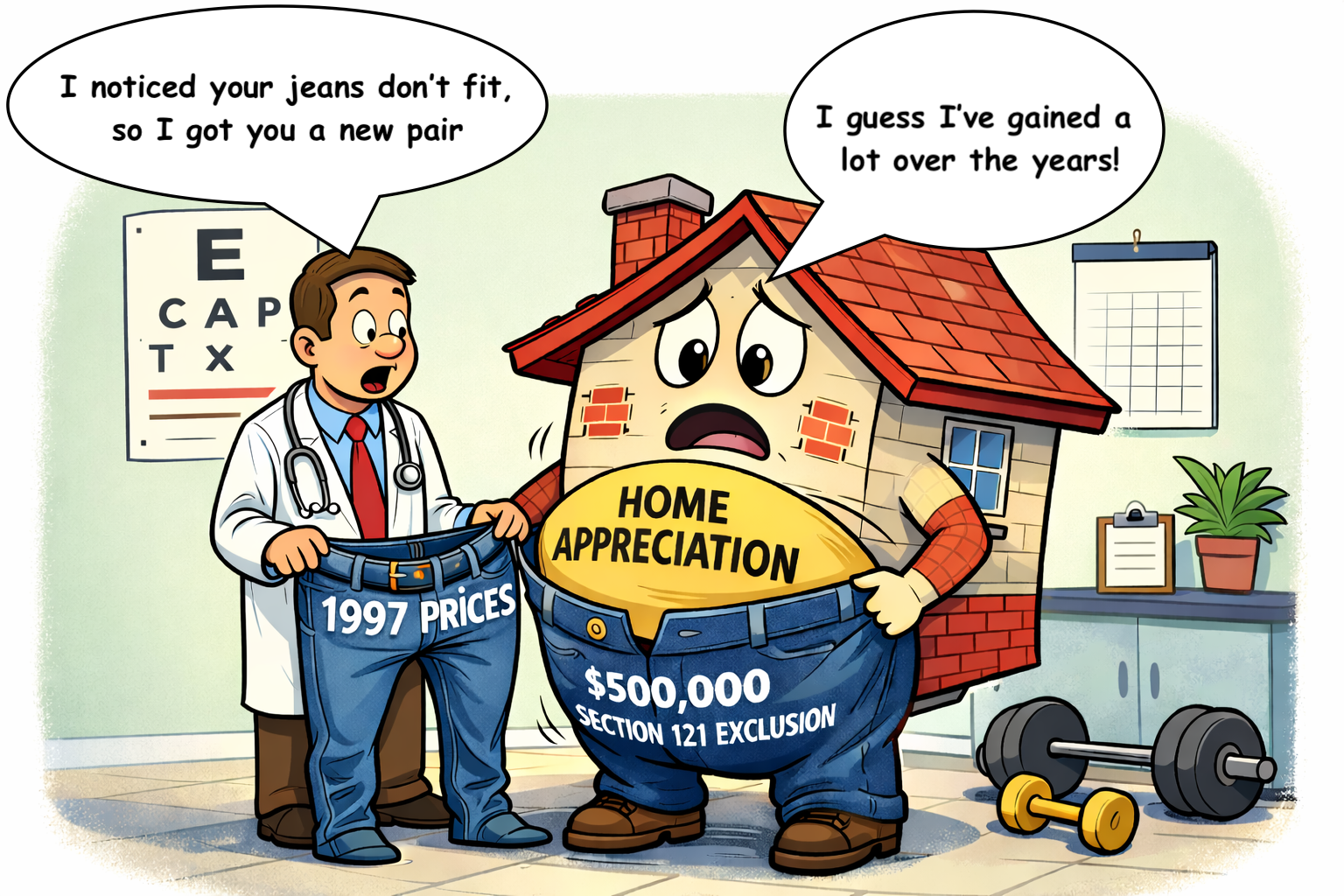

The $500,000 Home Sale Tax Break You Can Accidentally Throw Away

For most homeowners, the sale of a primary residence is one of the largest financial transactions they’ll ever make — and for many, it comes with one of the most generous tax benefits in the Internal Revenue Code.

That benefit is Section 121.

But Section 121 is also easy to misuse, misunderstand, or quietly forfeit.

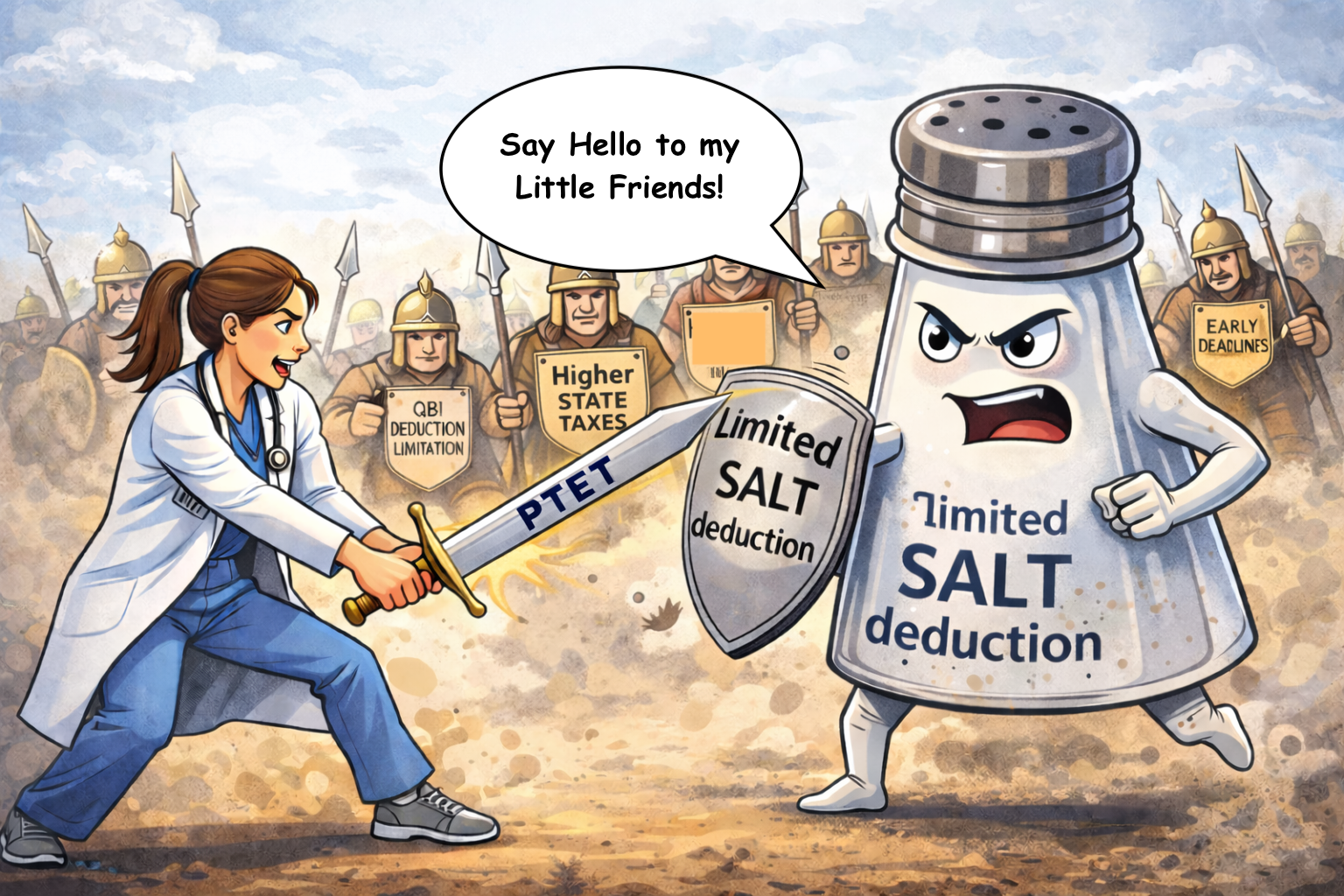

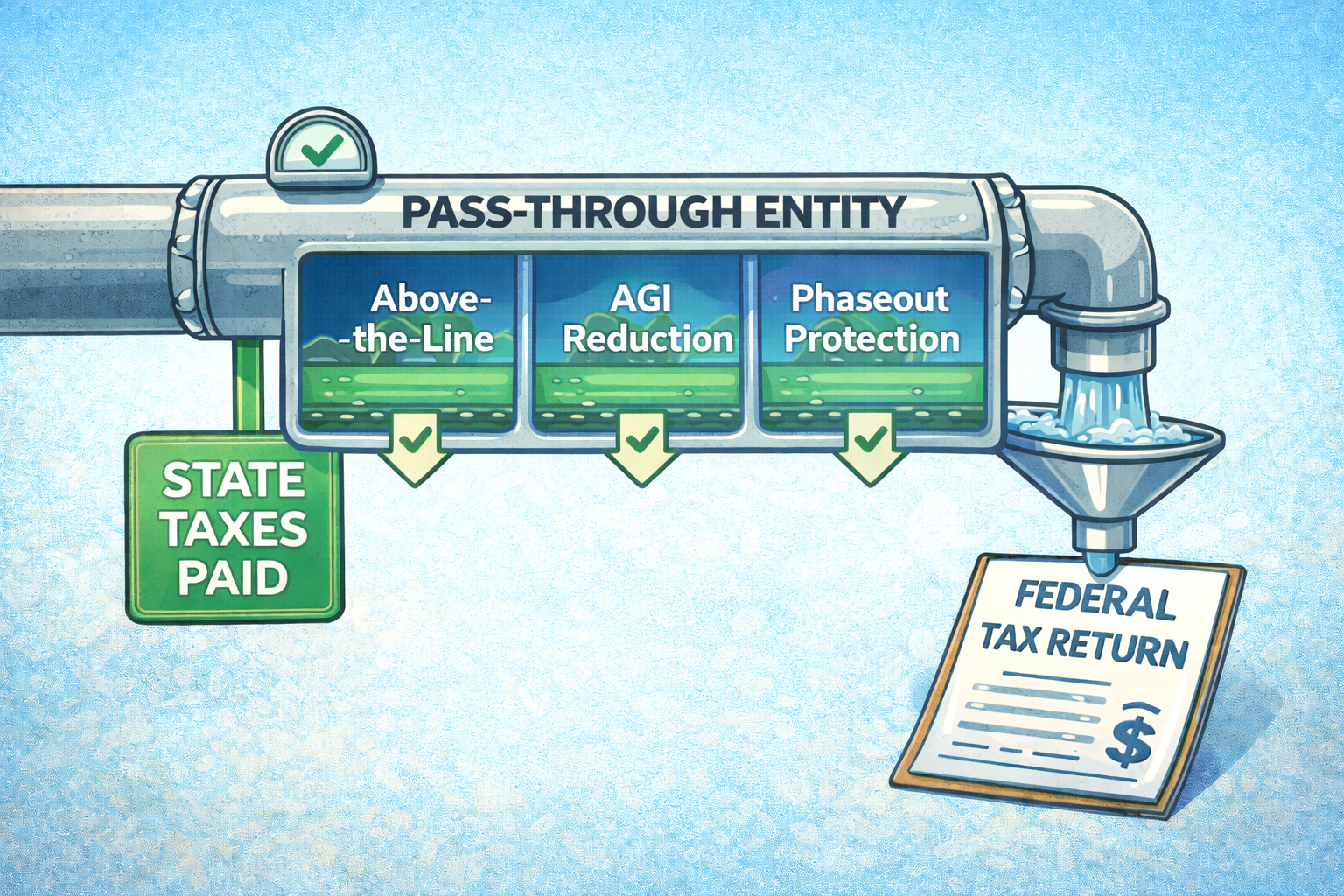

Pass-Through Entity Tax After OBBBA: The Fine Print That Can Cost You

In Part I, we looked at how the Pass-Through Entity Tax (PTET) can still save taxpayers money — even after the OBBBA loosened the SALT deduction rules. For the right taxpayer, deducting state taxes at the entity level and reducing AGI can be a meaningful win.

But the PTET is not uniform across states, and it’s not free of tradeoffs.

In this post, we’ll look at how the PTET works differently depending on where you live, the multi-state complications that catch people off guard, and a handful of pitfalls that can quietly erode the benefit.

Pass-Through Entity Tax After OBBBA: Still Worth the Trouble?

This is the first of a two-part series on the Pass-Through Entity Tax (PTET).

Today, we’ll focus on how the PTET can still save you money, even after the OBBBA relaxed some of the restrictions on deducting state and local taxes. In next week’s post, we’ll look at the downsides — including situations where the PTET can actually cost you more than it saves.

Should You Eat Ice Cream for Breakfast? Deciding Whether to Claim Accelerated Depreciation

Most people agree that eating ice cream for breakfast is a questionable life choice.

And yet… sometimes it happens.

Accelerated depreciation falls into the same category. It can be delightful in the moment, but if you don’t understand what you’re doing (or why you’re doing it), you may regret it later.

Should Parents Open “Trump Accounts” for Their Kids — or Is This Just Another Account to Forget?

A new type of account is about to enter the personal finance ecosystem: Trump accounts. The name alone has generated plenty of attention, but for parents, the more important question is whether these accounts actually make sense as part of a broader financial plan.

Your Tax Year Is Bigger Than Your Calendar Year

A common misconception I see — even among highly educated professionals — is the belief that everything on your tax return has to happen between January 1st and December 31st.

It doesn’t.

For physicians, business owners, and self-employed professionals, this timing flexibility is often the key to making aggressive tax planning actually work in real life.

Let’s walk through the major deadlines — and what actually needs to happen by each one.

Should You Hire Your Spouse? (And Will the IRS Thank You or Audit You?)

Few tax questions sound as deceptively appealing as: “Should I just hire my spouse?”

At first glance, the idea seems clever. The work stays in the household, the money stays in the household — surely the tax benefits follow, too… right?

As with most clever ideas in tax planning, the answer is: sometimes, rarely, and only under the right circumstances. Hiring your spouse can be worthwhile, but it can also result in higher taxes, unnecessary payroll complexity, and zero net benefit.

Let’s walk through when this strategy makes sense, when it doesn’t, and what you should consider before adding your spouse to payroll.

Don’t Jump the Gun: Why You Should Wait Before Making 401(k) Employer Contributions

There is something irresistibly satisfying about funding a retirement account early — the same kind of joy you get from clearing your inbox, finishing charting before noon, or finding out your prior authorization actually went through. But when it comes to 401(k) employer contributions, going too early can create a tax mess that is far more painful than waiting until January.

Let’s walk through why timing matters more than you think — and why many physicians and small business owners should hold off on employer contributions until the year is officially over.