Is That Drive Deductible? The Rules Every 1099 Physician Should Know

Be sure to read to the end for a special trivia question!

For many self-employed physicians—especially locums, telehealth doctors, and those working at multiple sites—vehicle expenses are one of the most misunderstood deductions in the tax code.

IRS Publication 463 lays out the rules. The principles are straightforward, but the real value comes from understanding how to apply them in real life—and how to plan ahead.

Let’s walk through it.

Personal vs Business Miles

The IRS allows a deduction only for business miles, not personal miles.

Business miles generally include:

Driving between job sites

Driving from your office (including a qualifying home office) to a work location

Driving to from a primary business location meet patients, clients, or vendors

Driving to the bank, pharmacy, or other business errands

Personal miles include:

Commuting

Grocery runs

Driving your kids to school

Weekend trips

If you drive 12,000 miles in a year and 4,000 of those are business miles, then your business-use percentage is 33%. That percentage becomes important if you use the actual expense method (we’ll discuss that later).

The Commuting Rule

One of the most important rules in Pub 463:

Driving from home to your regular place of work is commuting—and commuting is not deductible.

It doesn’t matter if:

The drive is long

You work odd hours

You are on call

You are self-employed

If the location is your regular workplace, the drive there is commuting.

This rule may be surprising. If the only driving you do related to your work is from your residence to the hospital in town (and you don’t have a qualifying home office), you can’t deduct any of your driving expense.

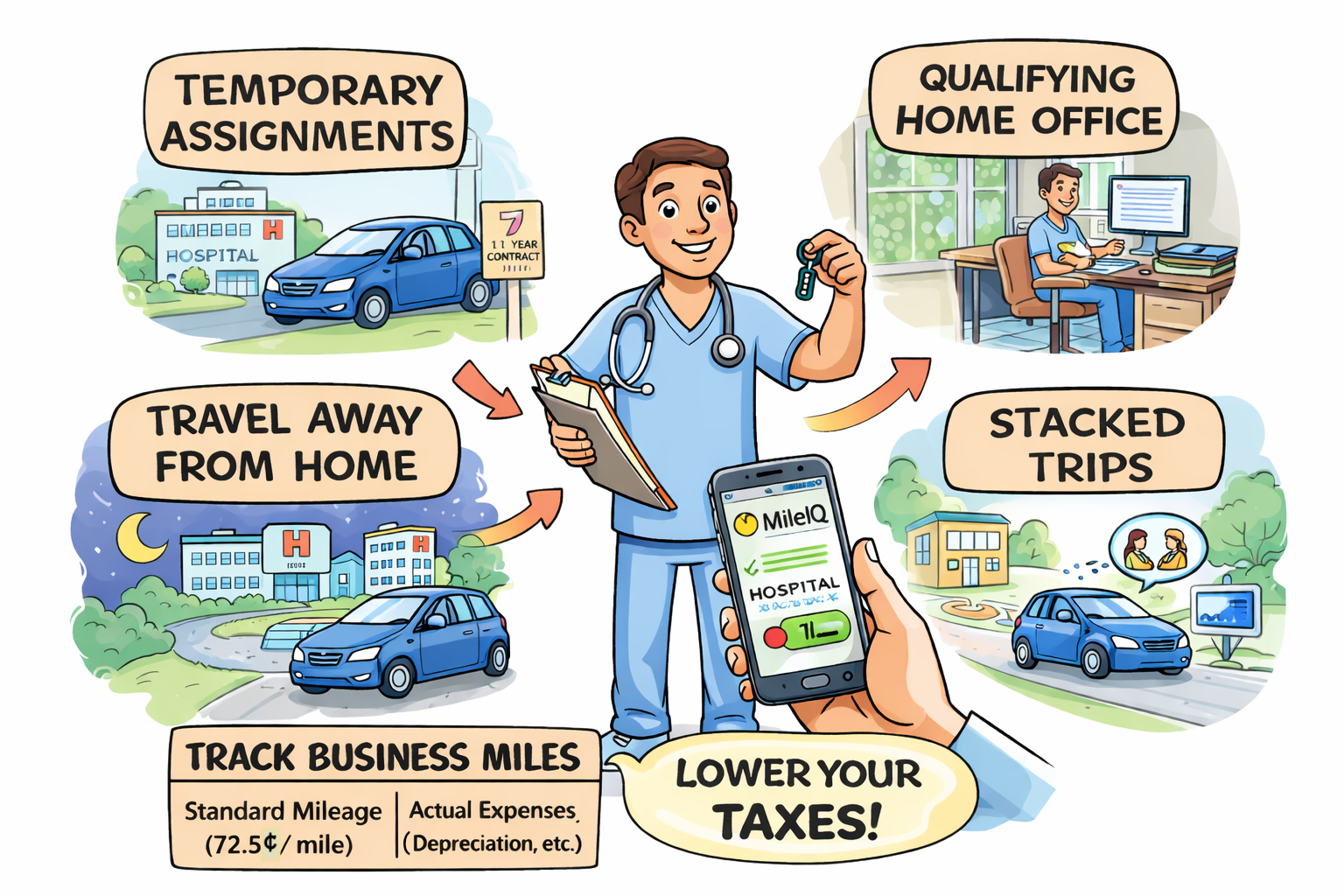

Temporary Job Assignments

Here’s where things get interesting for locums physicians.

Driving to a temporary work location can be deductible if it is outside the metropolitan area in which you live. This is because your “tax home” doesn’t change as the result of a temporary assignment. This language is taken directly from Pub 463:

”If your assignment or job away from your main place of work is temporary, your tax home doesn’t change. You are considered to be away from home for the whole period you are away from your main place of work. You can deduct your travel expenses if they otherwise qualify for deduction. Generally, a temporary assignment in a single location is one that is realistically expected to last (and does in fact last) for 1 year or less.”

A job is generally considered temporary if:

It is realistically expected to last one year or less, and

It does not become indefinite.

If the work is expected to last longer than a year, it’s no longer temporary. If you initially expect the term to be one year or less, but the length of the assignment subsequently changes, then the travel expenses cease to be deductible after the assignment no longer meets the definition of temporary.

This is common in locums arrangements where contracts are short-term or renewable.

If you drive from your tax home to a temporary assignment, those miles may be deductible—especially if you are not commuting to a regular permanent work location.

The Impact of a Qualifying Home Office

A qualifying home office changes the analysis significantly.

If your home office qualifies under IRS rules (regular and exclusive use, principal place of business or administrative center), then:

Your home becomes a business location.

That means:

Driving from home to another work site can become business miles rather than commuting.

This is one of the most powerful but underused planning tools available to self-employed physicians. However, the stipulations for a qualifying home office are strict and should not be brushed aside.

Traveling Away From Home

Driving expenses can also be deductible when you are traveling away from your tax home.

To qualify:

The trip must require sleep or rest, and

It generally involves more than one workday.

Examples:

Driving to another city for a multi-day assignment

Locums work requiring overnight stays

In these cases, mileage to and from the location may be deductible, along with lodging and meals (subject to rules).

A same-day trip typically does not qualify as travel away from home.

How to Track Business Miles

Good documentation is essential.

The IRS expects records showing:

Date

Destination

Business purpose

Miles driven

The easiest way to do this today is through a mileage tracking app.

One of the most commonly used options is MileIQ, which:

Automatically tracks drives

Lets you classify trips

Produces reports at year-end

This is far easier than reconstructing mileage from memory, which rarely holds up well in an audit.

Planning Strategies to Lower Taxes

Knowing the rules is helpful. Planning around them is where the real savings happen.

1. Set Up a Home Office (If It Qualifies)

If you legitimately qualify, a home office can:

Convert many commuting miles into business miles

Increase deductible mileage significantly

This is especially valuable for:

Telehealth physicians

Locums physicians

Physicians managing administrative work from home

But remember: the home office must meet IRS requirements. This is an area where documentation matters.

2. Prefer Temporary Assignments When Possible

Temporary work locations often create:

Deductible mileage

Travel deductions

Lodging and meal deductions

Permanent positions rarely provide these opportunities.

3. “Stack” Your Trips

If you don’t have a home office, try to structure trips so that:

You visit multiple sites or complete errands in one trip

You drive between business locations rather than always from home

Driving between business locations is deductible even when commuting is not.

4. Make Sure Out-of-Town Trips Qualify

If you drive out of town:

Make sure the trip requires sleep or rest

Make sure it spans more than a single workday

Otherwise, what feels like travel may be treated as commuting.

5. Standard Mileage vs Actual Expenses

Each year, you can generally choose between:

Standard mileage method

72.5 cents per mile (2026 rate)

Simple recordkeeping

Often best for fuel-efficient vehicles or moderate mileage

Actual expense method

Gas (or electricity)

Insurance

Repairs

Depreciation

Registration

Lease or loan interest (business portion)

To compare methods, you need:

Total miles driven

Business miles

Business-use percentage

One important detail:

Even if you use the standard mileage method, you may still deduct:

Parking fees

Tolls

Business portion of auto loan interest

Business portion of property taxes on the vehicle

TaxSmart Takeaway

Vehicle deductions are not about finding loopholes—they are about understanding definitions.

The biggest drivers of savings usually come from:

A qualifying home office

Temporary assignments

Traveling away from your tax home

Proper mileage tracking

Choosing the right deduction method

For many self-employed physicians, these factors can mean thousands of dollars in tax savings each year—not because the rules are aggressive, but because they are applied correctly.

Special Trivia Question!

IRS Revenue Ruling 1999-7 established that traveling from one’s home to a temporary work location, outside of a taxpayer’s metropolitan area, is a deductible business expense.

How does this ruling define “metropolitan area?”

A. 25 miles from the taxpayer’s residence

B. 50 miles from the taxpayer’s residence

C. Anywhere outside the taxpayer’s Metropolitan Statistical Area

D. Any location that realistically requires more than an hour of driving

E. No definition is provided

Click here for the answer!