How Are Inheritances Taxed? (And How to Plan for Them)

Be sure to read until the end for a special trivia question!

Inheritances can cause major changes in your overall income tax, but the good news is that you have ample time to create a plan for them.

Most people don’t spend much time thinking about how an inheritance will be taxed—until it actually happens.

From a tax standpoint, inheritances are a bit counterintuitive. In many cases, nothing dramatic happens right away, but over time—especially with retirement accounts—the tax consequences can be significant.

If you’re expecting to inherit assets (or already have), here’s how to think about it.

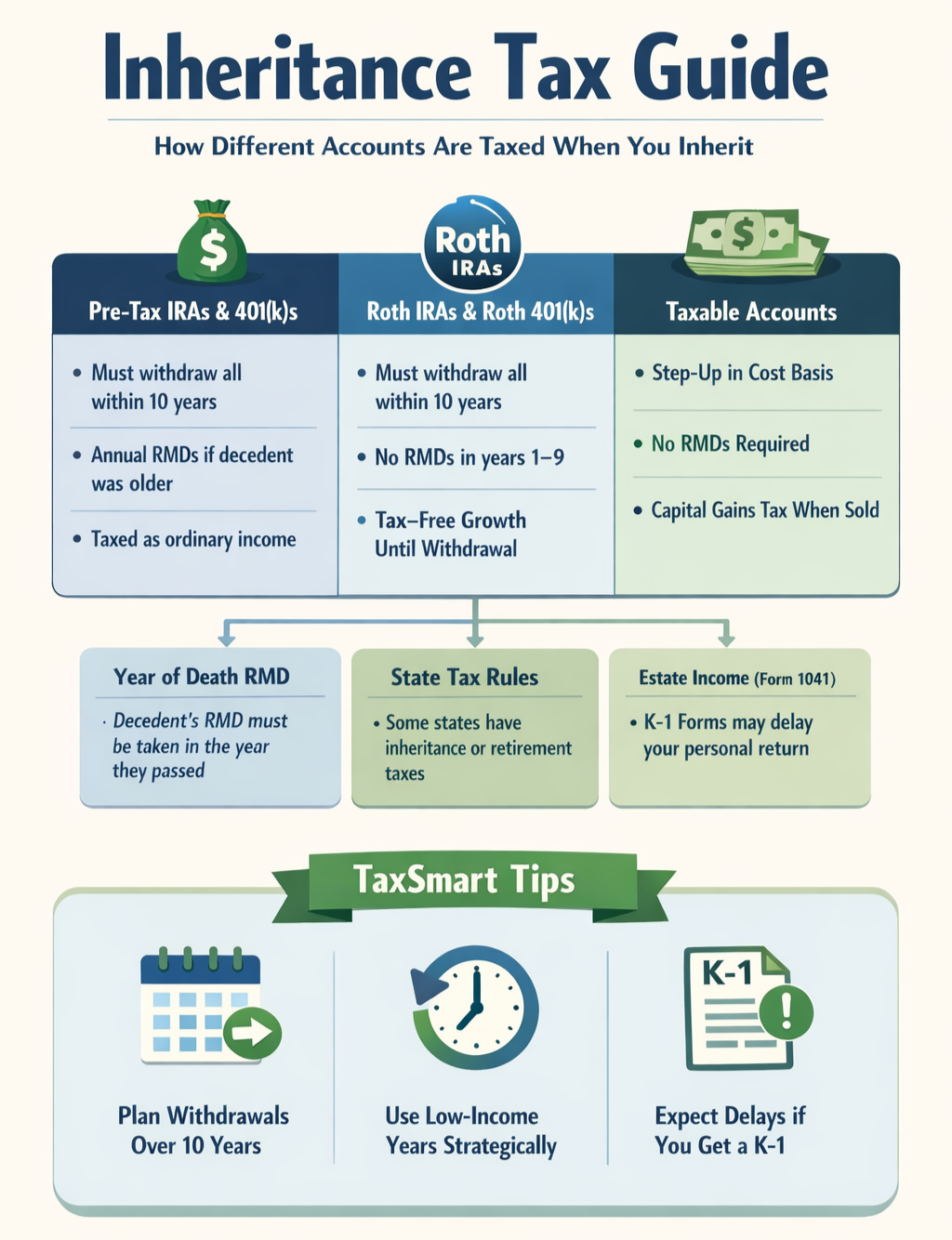

I. How Different Accounts Are Taxed on Inheritance

A. Pre-Tax IRAs and 401(k)s

After the passage of the SECURE Act, most non-spouse beneficiaries no longer have access to the “stretch IRA.”

Instead:

The account must be fully distributed within 10 years

If the decedent died on or after their required beginning date, annual distributions are also required during years 1–9

Each distribution is taxable as ordinary income

In other words, if your loved one left you a large pre-tax retirement account, you should expect your income to increase meaningfully over the next decade.

Why timing matters

You have flexibility in when to recognize that income within the 10-year window.

As a tax planner, I would:

Look at your current marginal tax rate (including surtaxes, phase-outs, and state taxes)

Compare it to expected future years

If you’re planning:

A sabbatical

Early retirement

Reduced clinical hours

Those lower-income years are often the best time to take distributions

Year-of-death RMD (easy to miss)

You also need to determine:

Did your loved one take their RMD in the year they passed away?

If not:

That RMD still needs to be taken

It is calculated as the decedent’s RMD for that year, using their age and the prior year-end account balance

It is taxable to you

This is separate from the 10-year rule and often overlooked.

One important limitation

Inherited pre-tax accounts:

Generally cannot be converted to Roth IRAs by non-spouse beneficiaries

B. Roth Accounts

Inherited Roth IRAs and Roth 401(k)s are also subject to:

The 10-year rule

However:

Distributions are generally tax-free

Most non-spouse beneficiaries are not required to take annual distributions during years 1–9

So what’s the strategy?

Since distributions don’t increase your tax liability:

The main goal is to maximize tax-free growth

For most people:

Take minimal or no distributions in years 1–9

Take the remaining balance in year 10

Why?

The money continues growing tax-free inside the Roth

Once withdrawn, future growth becomes taxable (dividends, capital gains)

C. Taxable Brokerage Accounts

When you inherit a taxable account:

You receive a step-up in basis

That means:

The cost basis resets to fair market value at death

If you sell immediately → little or no capital gain

Practical implications

No RMDs

No forced timeline

Can be merged with your existing brokerage accounts

For these reasons, taxable accounts are one of the most beneficial accounts you can inherit, owing to their flexibility and tax efficiency.

II. What to Expect in the Year of Death

There’s often confusion about what happens in the year your loved one passes away.

Final individual return

Your loved one will need a final Form 1040:

Married couples can still file jointly or separately

Same standard deduction applies

Estate tax (usually not an issue)

The federal estate tax exemption is now around $15 million per person

Most families will not need to file an estate tax return at the federal level (some states have more aggressive estate taxes).

Estate income tax return (Form 1041)

If assets remain in the estate and generate income:

The estate may need to file Form 1041

Filing threshold: $600 of gross income

Important nuance:

If retirement accounts pass directly to named beneficiaries, they typically do not generate income at the estate level.

If the estate is the beneficiary, distributions may be taxable to the estate and later passed through via K-1 to beneficiaries.

K-1 forms for beneficiaries

If the estate generates income:

You may receive a Schedule K-1.

This tells you:

How much income to report on your own return.

Practical issue (this happens a lot)

If a K-1 is coming:

You will likely need to file an extension.

Because:

The estate return is often prepared by a different professional.

It may not be ready before April 15.

III. Inheritance Tax and State Considerations

Federal level

No inheritance tax

(Separate from estate tax)

State inheritance tax

A handful of states impose one, but:

Many exempt close relatives (children, spouses).

Most people will not encounter this.

Still, it’s worth checking if:

You or your loved one lived in one of these states.

State taxation of inherited retirement accounts

This varies widely.

Some states:

Fully tax distributions

Others:

Offer partial or full exemptions

Example: Colorado

Colorado allows a subtraction for retirement income:

Age 55–64 → up to $20,000

Age 65+ → up to $24,000

This can include inherited retirement distributions.

State rules can materially impact planning, especially for large inherited IRAs.

Even if your tax advisor isn’t local, they should:

Know this matters.

Know how to research it.

IV. Other Things to Know

Pro rata rule

Inheriting a pre-tax IRA:

Does not trigger the pro rata rule for your own Backdoor Roth IRA.

HSAs (one of the worst to inherit)

If inherited by a non-spouse:

The account ceases to be an HSA

The entire balance is generally taxable in that year (with limited reduction for certain medical expenses paid after death)

This is one reason you don’t want to let your HSA grow indefinitely without ever using it.

Other accounts

Some accounts (529s, trusts, etc.) have their own rules, but:

The big drivers of tax impact are almost always:

Pre-tax retirement accounts.

Timing of distributions.

V. TaxSmart Takeaway

In most situations your taxes won’t change dramatically in the year you receive an inheritance.

However:

Inherited pre-tax retirement accounts must be emptied within 10 years.

This can significantly increase your tax liability over time.

What matters most

Timing distributions

Use lower-income years strategicallyUnderstanding RMD rules

Especially the year-of-death RMDCoordinating with the estate

Know if a K-1 is coming

Plan for potential extensions

An inheritance is not just a windfall—it’s a 10-year tax planning problem

Handled correctly, you can keep significantly more of it.

Handled poorly, you may give a large portion away unnecessarily.

Special Trivia Question!

This blog post simplified the rules for taxing inherited assets under the SECURE Act. It is written primarily with adult children in mind, who are considered “non-eligible designated beneficiaries” under the SECURE Act.

There is a separate category of “eligible designated beneficiary,” and these individuals receive more favorable treatment. There are five types of “eligible designated beneficiary.” Which of these is NOT an example of one of these?

A. Decedent’s surviving spouse

B. Decedent’s 22-year-old son, who is a full-time student

C. A beneficiary who is disabled

D. A beneficiary who is chronically ill

E. Decedent’s hairstylist, who was born five years after the decedent.

Click here for the answer!