Pass-Through Entity Tax After OBBBA: The Fine Print That Can Cost You

(PTET Series – Part II)

Read until the end for an infographic and trivia question!

The PTET is an effective weapon, but it needs to overcome more than just the SALT deduction limit

In Part I, we looked at how the Pass-Through Entity Tax (PTET) can still save taxpayers money — even after the OBBBA loosened the SALT deduction rules. For the right taxpayer, deducting state taxes at the entity level and reducing AGI can be a meaningful win.

But the PTET is not uniform across states, and it’s not free of tradeoffs.

In this post, we’ll look at how the PTET works differently depending on where you live, the multi-state complications that catch people off guard, and a handful of pitfalls that can quietly erode the benefit.

1. Not All PTETs Are Created Equal

The biggest misconception I see is assuming that every state treats the PTET the same way. They don’t.

Broadly, states fall into three buckets.

A. Refundable Credit (Most Favorable)

This is the cleanest and most taxpayer-friendly version.

Under this model:

The business pays the PTET

The owner receives a credit on their personal return

If the credit exceeds personal tax liability, the excess is refunded

In other words, you get 100% credit for what you paid, even if it’s more than your individual tax bill.

States that use this approach include:

Oregon

Illinois

Massachusetts

New York

This is obviously ideal. You’re not tying up cash, and you’re not forced to wait years to recover excess payments.

Not every state is quite this generous, though. Connecticut, for example, only allows a credit equal to 87.5% of the PTET paid — meaning some tax paid at the entity level is effectively lost.

B. Nonrefundable Credit

Under this structure:

You still receive a credit on your personal return

But if the credit exceeds your personal tax liability, the excess is carried forward, not refunded

This is less favorable from a cash-flow perspective.

Examples:

Arizona

California

Both states allow the excess credit to be carried forward for up to five years. That’s better than nothing — but it assumes you’ll have sufficient future income to actually use the credit.

If your income fluctuates, or you exit the business, those credits can linger longer than expected.

C. Income Exempted (Rather Than Credited)

Some states don’t provide a credit at all.

Instead, they:

Exempt the S-corp income on the personal return

Tax that income only at the entity level

This can be less favorable than a credit, especially if the PTET rate is higher than your marginal personal rate.

Example

Wisconsin imposes a 7.9% PTET.

But Wisconsin’s top individual rate of 7.65% doesn’t apply until income exceeds roughly $420,000. Below that threshold, marginal rates can be closer to 5.3%.

In that case:

Paying PTET at 7.9% can actually cost more than paying personal tax

Even though the income is exempted on the personal return

Other states using income subtraction rather than credits include:

Georgia

Arkansas

This is an area where the PTET can quietly turn from a benefit into a drag.

D. Other State-Specific Quirks

Some states add extra layers of complexity.

Colorado is a good example.

If you make Colorado’s SALT Parity election, the state taxes not only your business income — but also the Qualified Business Income (QBI) deduction you took on the federal return.

Example

You claim a $10,000 QBI deduction

At a 24% federal bracket, that saves $2,400

Colorado taxes that deduction at 4.4%

Result: Colorado tax increases by $440

The PTET may still be beneficial overall, but this kind of interaction needs to be modeled — not guessed.

2. Multi-State Complications

Things get more interesting when income crosses state lines.

Without PTET

If a business earns income in multiple states and does not elect PTET:

The owner’s home state usually allows a credit for taxes paid to other states

This generally avoids double taxation

With PTET

When taxes are paid at the entity level, the home state may — or may not — allow a credit for those taxes.

Example:

The same credit may not apply to partnership income

Even more challenging:

Not all states have issued clear guidance

Some rules differ by entity type

Some situations depend on administrative interpretations rather than statutes

This is an area where assumptions can get expensive. If you have multi-state income, this is something your tax professional should explicitly verify.

3. Deadlines Matter (More Than You Think)

Unlike itemized deductions, the PTET often requires early action.

In many states:

You must make the election early in the year

Or make an estimated PTET payment

Waiting until filing season may be too late

Examples:

Miss the deadline, and the option is gone — regardless of whether it would have saved you money.

4. Other Pitfalls to Keep in Mind

Even when the PTET works, it can have side effects.

PTET Reduces Qualified Business Income

PTET payments reduce federal business income.

That means:

QBI is lower

The 20% QBI deduction may also shrink

Example

PTET paid: $5,000

Federal tax savings at 24%: $1,200

QBI deduction reduced by $1,000

Lost tax benefit at 24%: $240

You still come out ahead — but not by the full $1,200.

In some cases, especially when SALT limits aren’t binding, it may actually be better to deduct state taxes as an itemized deduction, since that does not reduce QBI.

TaxSmart Takeaway

The Pass-Through Entity Tax can still be a powerful planning tool — but it’s not universal, automatic, or harmless.

Whether it helps or hurts depends on:

Your state’s PTET mechanics

Refundable vs nonrefundable credits

Income exemption rules

Multi-state sourcing

Timing and cash flow

QBI interactions

The PTET rewards taxpayers who plan ahead and punishes those who assume.

In short:

This is not a box you check — it’s a strategy you model.

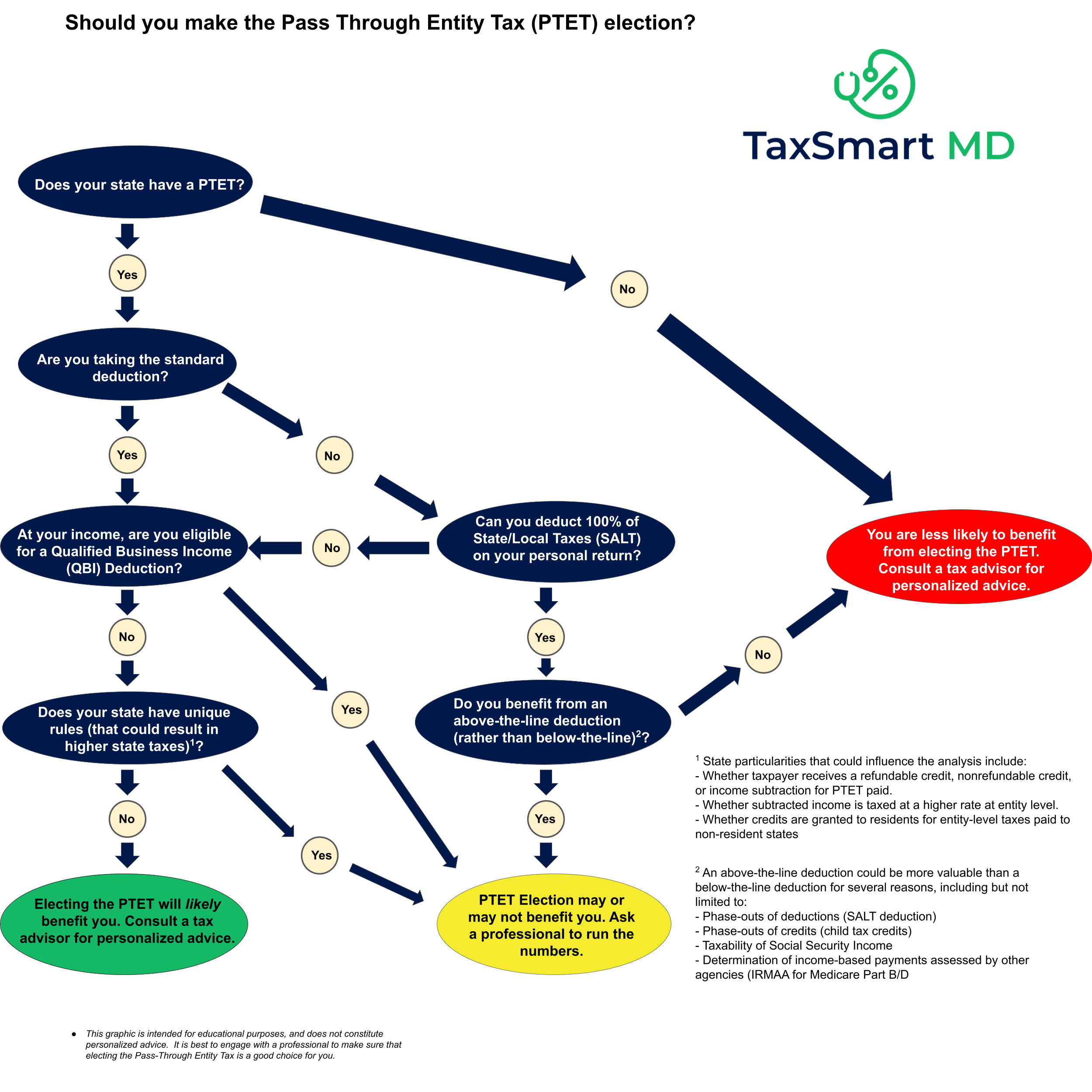

Visual Flowchart for PTET Election

When you decide whether or not to elect the PTET, there are numerous considerations to weigh. Hopefully this flow chart helps you evaluate them.

Special Trivia Question!

Which state has the highest PTET tax rate?

A. California

B. New Jersey

C. New York

D. Texas

Click here for the answer!