The $500,000 Home Sale Tax Break You Can Accidentally Throw Away

(Why Section 121 Is a Good Reason Not to Become an Accidental Landlord)

Read to the end for a Trivia Question!

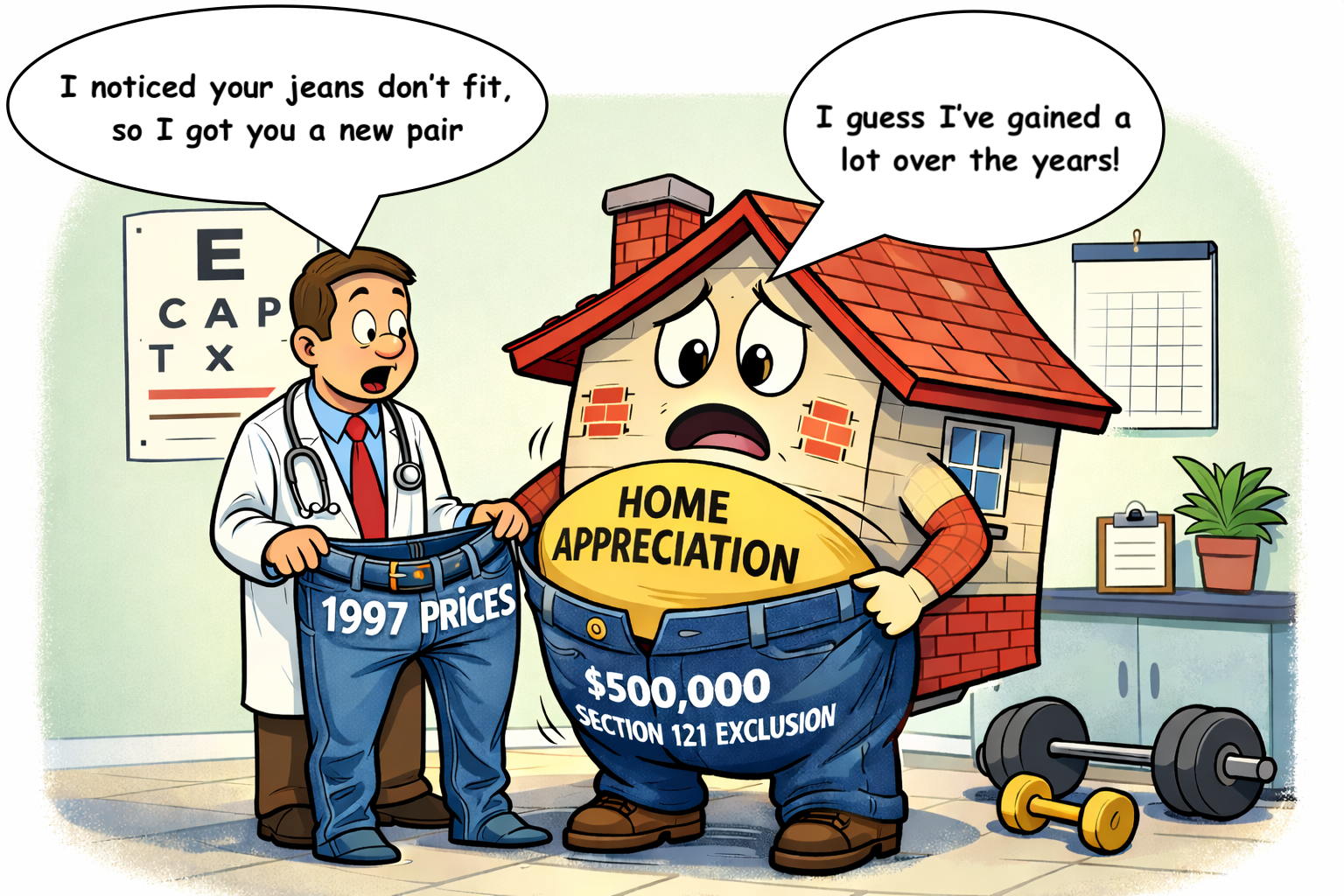

Nobody told you that your clothing size isn’t indexed to inflation.

For most homeowners, the sale of a primary residence is one of the largest financial transactions they’ll ever make — and for many, it comes with one of the most generous tax benefits in the Internal Revenue Code.

That benefit is Section 121.

But Section 121 is also easy to misuse, misunderstand, or quietly forfeit. One of the most common ways this happens is when a homeowner moves out and casually turns their old home into a rental — becoming an accidental landlord — without fully appreciating the long-term tax consequences.

Let’s break this down.

Part I: The Section 121 Exclusion (The Basics)

Section 121 allows homeowners to exclude a significant amount of capital gain when they sell their primary residence.

$250,000 of gain can be excluded if you’re single

$500,000 of gain can be excluded if you’re married filing jointly

This exclusion applies only to your primary residence, not a vacation home or investment property.

The ownership and use tests

To qualify for the full exclusion, you must meet both of the following tests:

Ownership test – You owned the home for at least two years

Use test – You lived in the home as your primary residence for at least two years

Importantly, those two years do not have to be consecutive.

The lookback rule

There’s also a two-year lookback test:

You can only use the Section 121 exclusion once every two years

If you claimed it on a prior home sale, you generally must wait two years before claiming it again

When all these conditions are met, Section 121 can eliminate capital gains tax entirely on what would otherwise be a very large taxable gain.

Part II: What to Do When It’s Time to Move or Upgrade

When homeowners experience a change in circumstances — a new job, a growing family, a move to another city — they often face a familiar choice:

Do I sell my old home, or do I turn it into a rental?

Whether the property is actually a good investment is a separate question (and one we won’t tackle here). But from a tax standpoint, there’s a major issue to be aware of.

The three-year clock

Once a home stops being your primary residence, the Section 121 exclusion doesn’t disappear immediately — but it does start ticking down.

If you sell the property within three years of moving out, you may still qualify for the exclusion (assuming the other tests are met).

After that:

The home is no longer treated as a primary residence

The Section 121 exclusion is generally lost

Any gain becomes subject to capital gains tax

Why this matters

Depending on appreciation, this can mean a six-figure tax bill down the road — on a property that would have been largely tax-free if sold earlier.

Now, there are situations where this isn’t a problem.

If you plan to:

Hold the property until death, and

Pass it to heirs who receive a step-up in basis

Then neither you nor your heirs will pay capital gains tax if the property is sold shortly after inheritance.

But if you:

Grow tired of being a landlord, or

Need to sell the property to fund retirement or long-term care

Then Section 121 suddenly becomes very relevant again — except it’s no longer available.

Part III: How to Make the Most of the Section 121 Exclusion

When you sell a home, the capital gain is calculated as:

Sale price – basis = capital gain

The higher the basis, the lower the taxable gain.

So what increases basis (or reduces gain)?

1. Closing costs when you bought the home

Certain purchase-related closing costs increase basis. This is why it’s important to keep your original closing statement, even if it’s decades old.

2. Seller-paid closing costs

Closing costs you pay when selling reduce the effective sale price, which also reduces capital gain.

3. Capital improvements

Capital improvements increase basis. The IRS generally defines these as projects that:

Add to the value of the home

Prolong its useful life, or

Adapt it to new uses

This does not include routine repairs.

For example:

Replacing a few shingles → repair

Replacing the entire roof → capital improvement

The line can be blurry, and a tax advisor can help with classification. The key takeaway is simple:

keep records. Receipts, invoices, and descriptions matter.

Part IV: Section 121 in Action (and Its Limits)

Section 121 can save homeowners well over $100,000 in capital gains taxes. But its usefulness is constrained by two major realities.

1. The exclusion hasn’t changed since 1997

The $250,000 / $500,000 limits were enacted in 1997 and have been frozen ever since.

Over the last 28 years:

Cumulative inflation has exceeded 100%

Home prices in many markets have risen far faster

If the exclusion were indexed to inflation, it would be more than double today.

2. No cost-of-living adjustment

The exclusion is exactly the same:

In rural North Dakota

And in downtown San Francisco

That makes planning much more important in high-appreciation or high-cost areas.

The Rental Dilemma

Here’s a common scenario:

You move out of your home and convert it to a rental. Five years later, you sell it.

Result:

The Section 121 exclusion no longer applies

You could owe $100,000+ in capital gains taxes

If you had sold immediately:

The gain may have been fully excluded

In some cases, a better strategy is:

Sell the primary residence while Section 121 still applies

Then buy a similar property as an investment

This effectively:

Locks in the tax-free gain

Resets your basis to current market value

Reduces future taxable appreciation

Should You Move Once You’ve “Used Up” the Exclusion?

There are obviously many non-tax factors that go into deciding where to live. But Section 121 is worth keeping in mind once appreciation approaches the exclusion limit.

Example

You buy a home for $400,000 in 2010

After improvements, your basis is $500,000

The home is now worth $1,000,000

Any further appreciation will eventually be taxable when you sell.

If:

Home prices rise 5% annually, and

Capital gains tax is 15%

That’s effectively:

$7,500 per year in future tax exposure

($1,000,000 × 5% × 15%)

Is it worth moving to avoid that? Maybe — maybe not. But it’s a question worth asking.

If you move and buy a new home, your basis resets. If you stay until death, the step-up in basis makes the issue irrelevant. The problem arises when plans change unexpectedly — which they often do.

TaxSmart Takeaway

Section 121 is a powerful benefit — but only when you sell

Converting a primary residence into a rental can quietly forfeit that advantage after a few years

Keeping accurate records increases basis and reduces capital gains

Know when you’re approaching the $250k / $500k limit

Keep Section 121 in mind whenever you anticipate a move, upgrade, or lifestyle change

Becoming a landlord isn’t inherently bad — but becoming an accidental landlord without understanding the tax tradeoffs can be very expensive.

Special Trivia Question!

The Section 121 exclusion is usually all-or-nothing, and you don’t get a partial exclusion if you only qualify for one year out of the two-year ownership and use requirement.

However, the IRS defines some exceptions that will let you qualify for a partial exclusion. Which of these does NOT qualify for the partial exclusion?

A. Having four children over the course of ten years

B. Divorce or legal separation

C. Health-related move

D. Change in employment (over a minimum distance)

E. Unaffordability due to a change in employment

Click here for the answer!