Time To Buy a Home? Here’s What Actually Happens to Your Taxes

Be sure to read to the end for a special trivia question!

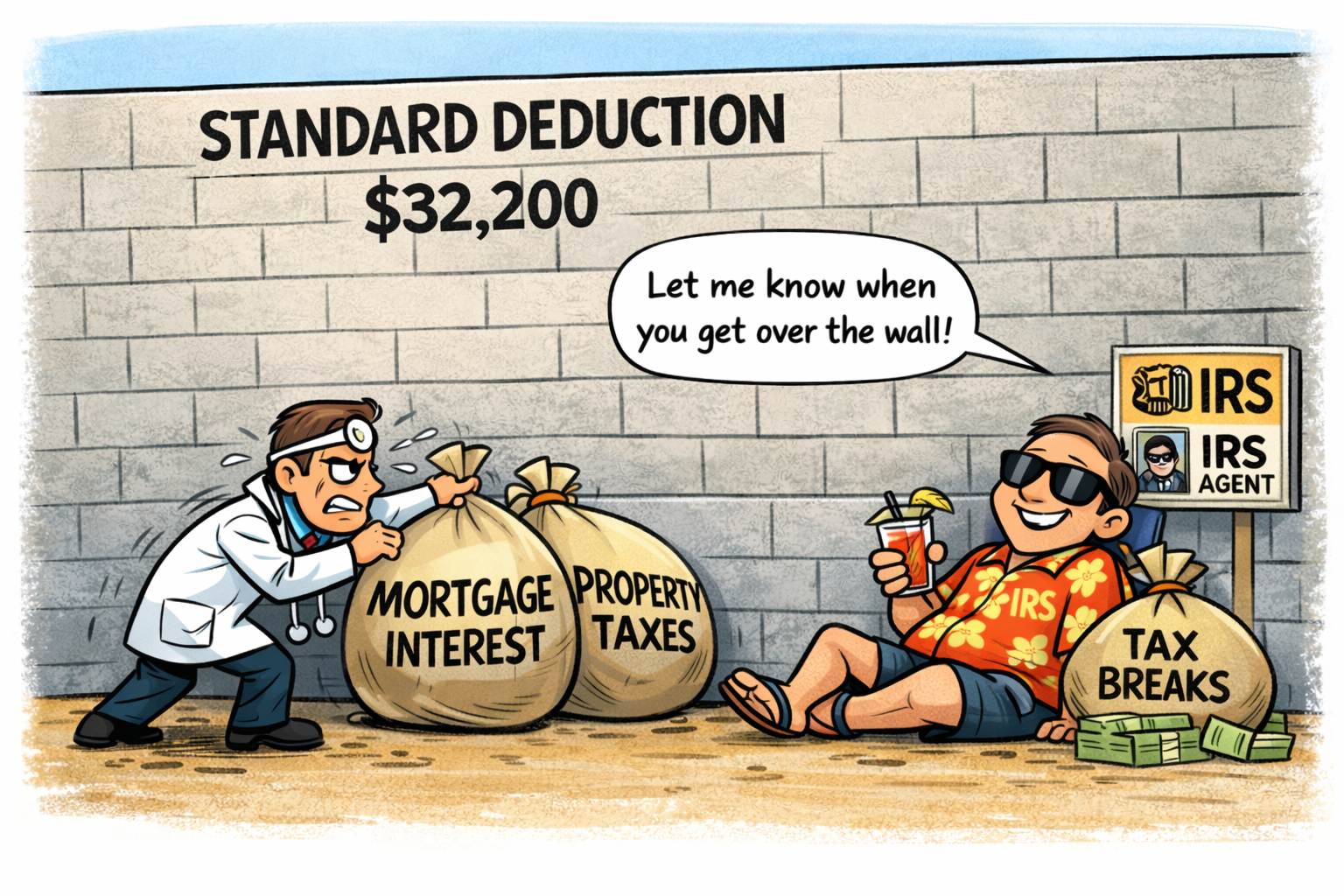

The standard deduction is a high hurdle to clear, but physicians (especially those with incomes under $500k) may have much taller ladders.

For most physicians, the decision to buy a home is driven by lifestyle, not taxes.

That said, once you cross into higher income levels, the tax treatment of homeownership can become meaningful—especially when itemized deductions come into play.

This post walks through what actually changes when you go from renting to owning, and where the real planning opportunities exist.

Part I – Deductible Expenses When You Own a Home

Owning a home introduces a new category of deductions that simply don’t exist when renting. This is because you can’t deduct rent as an itemized deduction.

Home Mortgage Interest

Mortgage interest is deductible under Internal Revenue Code §163(h), but only up to:

$750,000 of acquisition debt (federal limit)

Some states, such as California, allow higher limits at the state level.

This means:

A $750k mortgage → fully deductible interest

A $1M mortgage → only ~75% of the interest is deductible

Points (Prepaid Interest)

“Points” are simply prepaid mortgage interest.

They may be:

Fully deductible in the year paid (in certain purchase scenarios), or

Amortized over the life of the loan

This creates a planning lever we’ll revisit later.

Property Taxes

Property taxes are deductible under Internal Revenue Code §164, but subject to:

$40,000 cap in Deductible State and Local Tax (for most taxpayers, once their Modified Adjusted Gross Income exceeds $500k, this phases down to a cap of $10,000).

This includes:

State income taxes

Property taxes

Many physicians utilize this entire amount ($40,000 if MAGI < $500k, or less at higher incomes), regardless of home ownership.

Part II – How Closing Costs Are Treated

Most closing costs are not currently deductible. Instead, they are added to the basis of the home.

This includes:

Title fees

Recording fees

Legal costs

Why this matters:

When you sell the home:

Higher basis → lower capital gain

Lower gain → less tax

This is a long-term tax benefit, not an immediate one. (Note - this may be moot if you can exclude all capital gains from your home sale).

Part III – Planning Considerations

Here are some steps you can take to deduct as much mortgage interest and property tax as possible.

A. Keep the Loan at or Below $750k

If your mortgage is:

≤ $750k → all interest deductible

>$750k → some interest lost

Practically, I don’t think you should let this dictate the price range of your home purchase. However, if you’re going to save for a downpayment, you may want to see how much you can save in order to bring the mortgage loan down to $750k, or as close as you realistically can.

B. Maximize the Gap Between Standard and Itemized Deductions

The mortgage interest deduction only matters if you itemize your deductions. So the real question is:

How far above the standard deduction can you get?

Planning considerations:

It may be more valuable to have mortgage interest in years where:

SALT is fully usable

Income doesn’t phase down the maximum deductible SALT taxes

You take a larger deduction for charitable donations (for instance, in a year when you bunch donations).

If you only generate a small amount of mortgage interest:

You may not exceed the standard deduction at all

Using Points Strategically

Prepaying interest via points can:

Pull future deductions into the current year

Increase itemized deductions in a high-value year

This is particularly powerful when:

One year has unusually favorable deduction treatment

Future years are expected to be less favorable

Conversely, paying points is less valuable in a year where your total itemized deductions is less than, or close to your standard deduction.

C. Timing (within the year) Matters More Than People Think

If you buy late in the year, you may only have a few months of interest, which may not be enough to exceed the standard deduction.

If you buy earlier, you’ll pay more interest, which may get you “over the hump.”

Part IV – Example

Let’s walk through a real-world scenario.

Dr. SALT and Dr. Pepper are married physicians filing jointly. Dr. SALT has been out of training for a couple of years, while Dr. Pepper is graduating from residency this year (2026).

Dr. SALT income: $300,000

Dr. Pepper:

$100k (prior year)

$200k (current year)

$300k (next year)

They pay:

>$40,000 in state income taxes annually

No meaningful charitable contributions

Standard deduction:

$32,200 (2026)

$33,000 (2027) (assumed; IRS hasn’t released the inflation-adjusted numbers for 2027 yet)

Planned mortgage:

$700,000

Option A – Buy in 2026

SALT deduction = $40,000

Already exceeds standard deduction

Result: All mortgage interest is deductible

Option B – Buy in 2027

Income rises to ~$600k

SALT deduction limited to $10,000

Now:

Standard deduction = $33,000

SALT deduction = $10,000

Result:

First ~$23k of interest provides no incremental benefit

Only excess above that is “useful”

Key Observations

In this example, buying in 2026 produces a larger tax benefit.

In 2027 and beyond, ameaningful portion of interest may not be deductible in practice.

This couple may consider purchasing “points” in 2026 while 100% of interest is deductible.

This would accelerate deductions in a high-value year, and avoid “wasting” deductions in a lower-value year.

The conclusions are fact-dependent. You could easily “reverse” this scenario, such that the taxpayers benefit more by waiting. Timing and income trajectory matter significantly.

TaxSmart Takeaway

Buying a home is a personal decision, and it’s important not to let the tax tail wag the dog.

However, when you are truly on the fence, the tax treatment of mortgage interest and property taxes can shift meaningfully from year to year, based on income and the magnitude of other itemized deductions that are claimed. That shift can help guide the decision at the margins.

Itemized deductions remain one of the most valuable tax tools available to high-earning physicians. Thoughtful planning can ensure you actually benefit from them, rather than assuming you will.

Special Trivia Question!

If you buy a (second) vacation home, how much mortgage interest can you deduct?

A. Nothing more. You can only deduct interest on the primary home.

B. Both the primary and secondary homes share the $750k limit, which you apportion between both loans.

C. You get a separate $750k limit for the primary and secondary homes.

D. When you have more than one home, the limit increases from $750k to $1M.

Click here for the answer!